TL;DR

Faraday Future raised $25M in convertible notes for its robotics pivot. Half is locked in investor-controlled accounts.

Faraday Future raised $25M in convertible notes for its robotics pivot. Half is locked in investor-controlled accounts.

Faraday Future announced on Thursday that it has raised $25 million through convertible promissory notes, bringing its total financing over the past two months to $70 million. The company says the capital is sufficient to fund Phase 1 of its robotics business plan through the end of 2026. The stock, which trades on Nasdaq under the ticker FFAI, closed below $1 per share and is currently under a Nasdaq deficiency notice for failing to maintain the minimum bid price requirement.

The structure of the raise warrants attention. Of the $25 million, only $12.5 million goes directly into the company’s operating account. The remaining $12.5 million is deposited into control accounts held by the investors, and will be released to Faraday Future only upon satisfaction of certain undisclosed conditions. The press release describes “institutional investors’ confidence” in the company’s prospects but does not name any of the investors. The shares underlying the convertible notes are unregistered and subject to trading restrictions. The company’s own risk factors, filed with the SEC, acknowledge that it currently lacks sufficient share capital to execute its strategy and that obtaining stockholder approval for additional shares could result in “substantial additional dilution.”

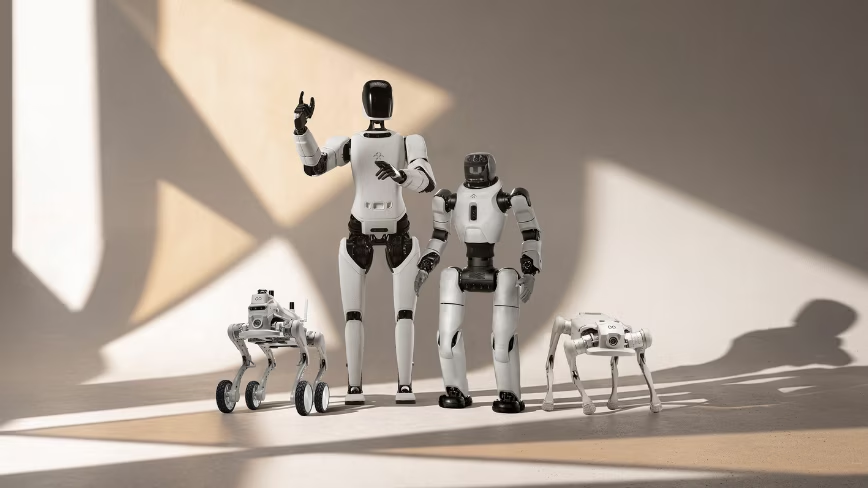

Faraday Future is pivoting from electric vehicles to what it calls “Embodied AI,” positioning itself as a physical AI company that delivers both humanoid and bionic robots. The company says it shipped 68 robots as of 30 April, with a full-year target of 1,500 units across four product lines aimed at education, security inspection, reception and guided tours, performance, and university research. Its Q1 2026 financial results reported that the robotics business achieved positive gross margins and generated ecosystem revenue, though the company did not disclose the total revenue figure in its press release.

The company also signed an MOU with RobotShop, a Canadian robotics e-commerce platform, as its first distribution partner for the robotics line. An MOU is a non-binding agreement and does not represent a committed order.

The corporate history is relevant context. Faraday Future was founded in 2014 by Chinese billionaire Jia Yueting, who has been at the centre of multiple financial controversies. The company went public via SPAC merger in 2021, after which the SEC launched an investigation into matters related to the PIPE and SPAC transactions. Wells Notices were issued to the company and certain executives. The SEC concluded its investigation in March 2026 with no enforcement action, which the company described as removing a “major historical overhang.” Separately, a special committee of independent directors had conducted its own investigation beginning in October 2021.

The EV side of the business has struggled to reach meaningful scale. Faraday Future’s FF 91, a luxury electric vehicle priced above $300,000, has been delivered in very small numbers since its 2023 launch. The company is now developing what it calls “EAI automotive robots,” essentially AI-enhanced vehicles, alongside its humanoid and bionic robot product lines.

The humanoid robotics market is attracting serious capital in 2026. Morgan Stanley doubled its forecast for China’s humanoid robot sales to 28,000 units this year. Unitree is filing for a $7 billion IPO after outselling Tesla on humanoid robots. 1X is shipping its NEO humanoid to US homes at $20,000 per unit. Mind Robotics, Rivian’s spinoff, raised $1 billion in under a year at a $3.4 billion valuation. In that context, Faraday Future’s $70 million in convertible debt financing, half of it conditional, positions the company at the very margins of a market being defined by companies with orders of magnitude more capital, more credible production capabilities, and more established technology.

The company’s own SEC filings list risk factors that include its “reliance on a single OEM for most of its robotics products,” competition from companies “with far superior experience, funding and name recognition,” the possibility that it may not maintain its Nasdaq listing, and the fact that its strategy requires stockholder approval for additional share issuance that could be substantially dilutive.

Faraday Future says it now has the room, for the first time in years, to shift financing decisions from “liquidity-driven to capital-structure-driven.” That framing reflects a company that has historically raised money on whatever terms it could get, when it could get them. Whether $70 million in convertible notes, with conditions attached, represents a genuine strategic inflection or another chapter in a long series of optimistic announcements followed by operational difficulty, is a question the market has been asking about Faraday Future for the better part of a decade.

Goldman Sachs projects 50,000 to 100,000 humanoid robots shipped globally in 2026. Faraday Future’s target of 1,500 units would represent a fraction of that market, but even that modest target requires execution from a company that has consistently struggled to deliver on its production commitments. The robotics pivot may be real. The capital may be sufficient for Phase 1. But the gap between announcement and delivery is where Faraday Future’s story has historically broken down.

Get the most important tech news in your inbox each week.