Over the past few years, a seismic shift has taken place in the world of retail banking. Traditional banks are now facing stiff competition from smartphone-only upstarts.

In the US, there’s Simple, and in the UK, there’s Monzo, Atom, Tandem, and Starling. By and large, these are all very much in startup mode. They don’t offer the full range of services that an old-school bank would.

But despite that, they’re soaring in popularity, particularly with millennials. This is largely because smartphone-only banks are more convenient, and tend to offer lower fees.

For the past two weeks, I’ve been using Monzo near-daily. It didn’t take long for it to convince me that it’s the future of banking. Here’s why.

The future is here, and it’s in my wallet

Most retail banks in the UK have a long and storied history. Barclays Bank, for example, was founded in 1690. But then again, most retail banks aren’t Monzo.

It started life in early 2015 in London under the name Mondo, and attracted a £5 million ($6.14 million) round of seed funding from Passion Capital – a London venture capital firm. In February 2016, it followed this up with a further £1 million ($1.23 million USD) funding round on crowdfunding platform Crowdcube. This was completed in just 96 seconds, and is believed to be the fastest crowdfunding campaign in history.

In August of this year, it finally secured a coveted banking license from the UK’s financial regulators. This meant that it was no longer just a pre-paid debit card. It’s a bank. Eventually it will be able to offer actual banking services, like overdrafts (line of credits) and transfers.

Another huge milestone for Monzo was two weeks ago, when it launched its Android app. Previously, it was exclusive to iOS. The Android version is yet to hit feature parity, but it’ll get there eventually.

Getting started with monzo

Opening an account with a traditional retail bank is an infuriating experience. First, you’ve got to make an appointment. Then you’ve got to bring a lifetime’s worth of documentation with you. If you make a mistake, or if the “computer says no”, you have to go back to square one and start again.

Monzo, on the other hand, is a surprisingly painless experience. It takes about two minutes to verify your identity, make the initial top-up (minimum £100), and request a debit card.

Your card should arrive within two working days. It contains a unique nine-digit number, which allows you to link the card to your account. Shortly after, your PIN number will be sent to you via SMS. Monzo recommends that you change this at an ATM.

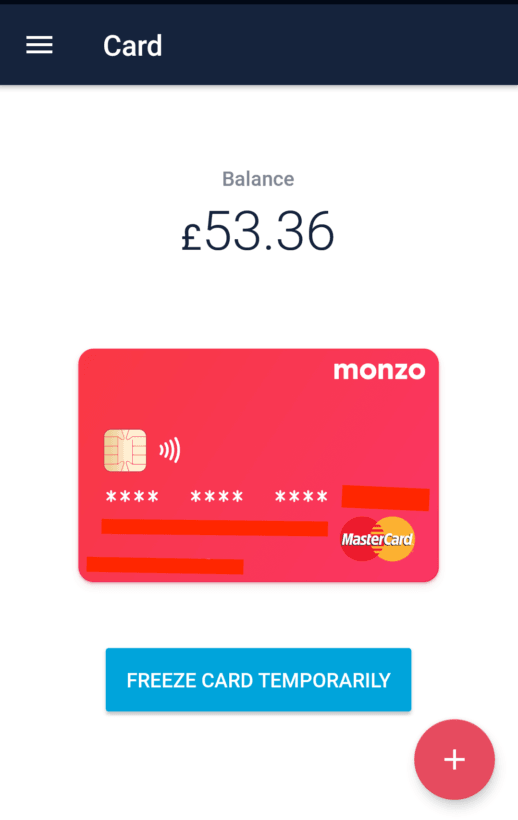

Then, you’re ready to start spending. The Monzo debit card is a Mastercard Debit, which means you’ll be able to use it virtually everywhere. In addition to the usual magnetic strip and chip-and-pin, it also comes with support for contactless payments.

Spending money with Monzo

The makers of Monzo are eager to emphasize that the product is still very much in beta mode. Indeed, if you sign up now, you’ll receive a card that says “Beta”. Consequently, it’s recommended that you carry around a backup debit or credit card with you.

This is pretty sage advice. Yesterday two card payments I tried to make were declined due to a computer glitch.

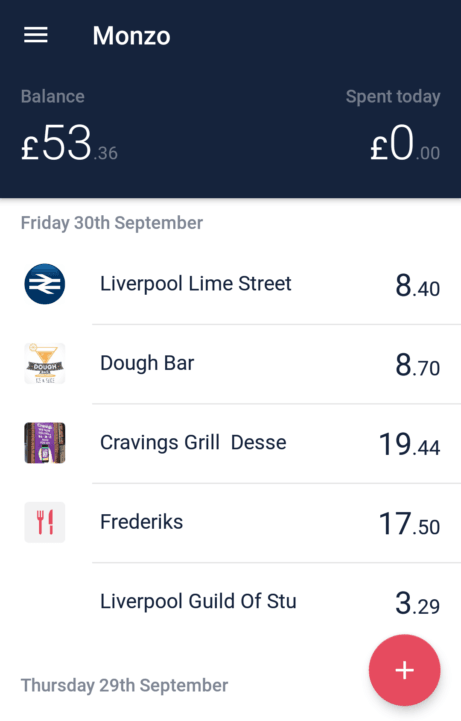

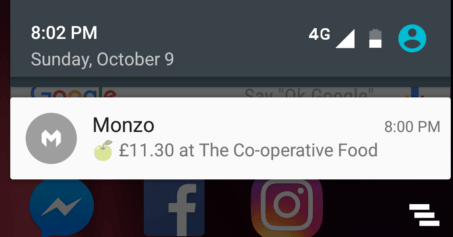

But by and large, I’ve used my Monzo card to make a variety of POS and contactless payments, and the bulk have gone through without a hitch. Once a transaction has been made, it immediately shows up on the app.

The Monzo app will also immediately send you a push notification.

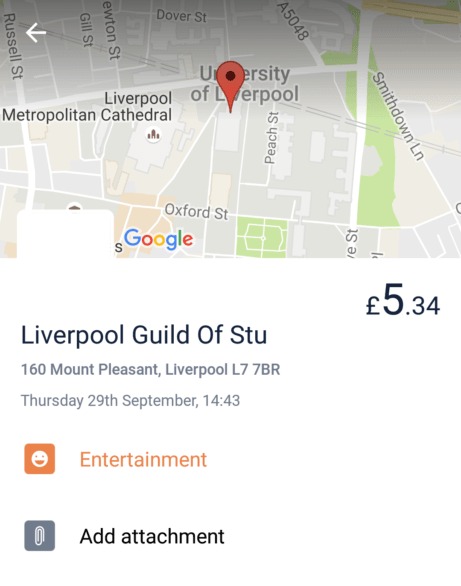

This makes it easier for you to budget. In the cold light of day how much you’re actually spending on Starbucks and cigarettes. You can also annotate each transaction with notes and photos, which is handy if you’ve trying to track business expenses.

These make it super easy to identify fraudulent transactions. And if someone does steal your Monzo card, you can freeze it with just a tap.

One of the my favorite things about Monzo is that it doesn’t charge any fees for international transactions. It doesn’t matter if you’re withdrawing cash or using a point-of-sale (POS) machine. There are no surcharges, and you’re charged the official MasterCard exchange rate.

This is pretty impressive. Most high-street banks charge ridiculous fees when you use your card abroad. My bank, for example, charges £1.50 (about $2), plus an additional 2.75 percent.

But it’s by no means a Monzo-exclusive feature. It’s something common across many of these un-banks. Simple, for example, doesn’t charge any international ATM withdrawal fees, although it does charge one percent on all international debit card transactions.

Exciting, early days

For Monzo, and many of the other so-called “challenger banks”, the future looks bright. People are clamoring to sign up, and there’s a real enthusiasm for what they’re offering.

But there are still a great many mountains for them to climb, both regulatory and technical. Will Monzo be able to offer a full banking experience without undermining the ease-of-use that makes it so popular? Will it be able to accomplish all the things that it wants to do, while sticking to the app-only model? Will it be able to turn a profit and become a sustainable business, while simultaneously refraining from charging the fees that banks do?

If it’s able to do all these things, the traditional retail banks should be worried.

Get the TNW newsletter

Get the most important tech news in your inbox each week.