The emergence of online resource-sharing and freelancing platforms have ushered in the new era of the gig economy. These services have made it possible to get or provide help on tasks and projects like never before. They’re now challenging traditional labor structures and models. In the U.S. alone, freelancers account for 35% of the workforce.

Upwork and Freelancer let you hire various talents remotely and coordinate projects from thousands of miles away. Uber and Lyft made it possible to make money for sharing your car, or find other people near you who can give you a ride. TaskRabbit helps you hire physical labor in your neighborhood for tasks such as moving and assembling furniture. Amazon’s Mechanical Turk provides you with cognitive human resources for tasks such as data labeling. Dozens of other websites provide similar services in other niches.

However, while these platforms have helped millions of people find jobs online, they suffer from very distinct problems. Lack of transparency, heavy taxing of income and delays in delivering earnings are some of the more prominent of these problems.

But more generally, all of these organizations are governed by hostile, centralized architectures. While a large crowd of freelancers and employers contribute to the value of these platforms, they don’t get a fair share of the profits. When using these services, freelancers, who cherish their freedom and like being their own boss, often feel they’re cogs in the wheels of a large organization that’s not giving them their due. That’s why they often find ways to cut deals outside the services to avoid paying the high commission rates.

Many experts believe blockchain, the technology that delivered Bitcoin and challenged the long-standing rule of banks and centralized financial institutions, can provide the answer to the dilemmas the online gig economy is facing.

The 💜 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol' founder Boris, and some questionable AI art. It's free, every week, in your inbox. Sign up now!

How blockchain makes the gig economy fairer

In essence, blockchain is a database that exists and is updated on thousands of computers. It’s transparent and available for all to see and impervious to tampering and other cyberattacks. Blockchain’s decentralized model enables secure peer-to-peer transactions without the need for intermediaries. It also makes it possible to execute smart contracts, software that runs on the network without the need for centralized application servers.

For the gig economy, the combination of blockchain transactions and smart contracts makes it possible to create freelancing and resource-sharing platforms where employers can find and hire employees, and compensate them without the need for a broker. Payments are made immediately in cryptocurrency without any delays.

There are now a handful of startups that are leveraging blockchain in online labor markets that give power and control to the participants. An example is CanYa, a decentralized marketplace of online services built on top of the Ethereum blockchain. CaYa enables employers and employees to interact peer-to-peer without the need for a intermediary party.

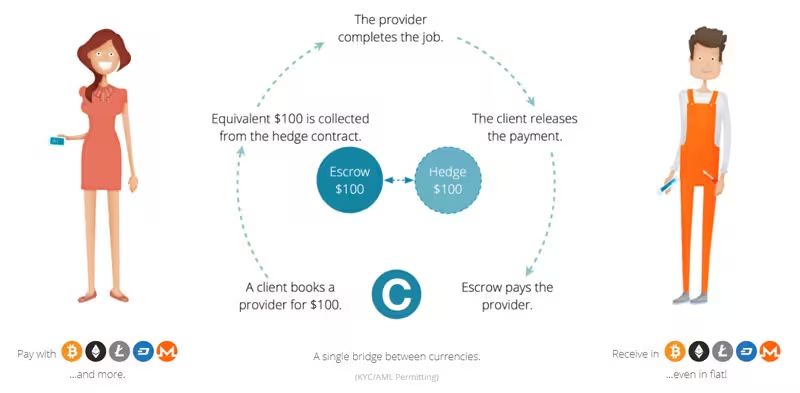

CanYa uses its own proprietary digital currency, the CanYa token. Employers can purchase CanYa to pay freelancers for their services. Every task creates a smart contract, which also performs the function of a decentralized escrow. When the work starts, the smart contract locks the agreed amount in tokens from the employer’s account. When both parties confirm the completion of the task, the smart contract automatically transfers the tokens to the employee’s address. This blockchain model ensures that freelancers receive their earnings immediately after completing their work. It also reduces fees by removing intermediaries. CanYa’s commission fee is 1%, a thin slice of UpWork’s 20%.

Similar platforms have emerged in other niche industries. For instance, Lazooz, a blockchain-based ridesharing application, aims to tackle some of the problems that centralized services such as Uber and Lyft haven’t been able to deal with. Winding Tree, a Switzerland-based non-profit, is the blockchain equivalent of Airbnb. Both platforms reduce third-party fees by a large extent.

Another way that blockchain can improve freelancing platforms is the use of anonymous crowd wisdom. Coinlancer, another decentralized freelancing platform, uses blockchain and the judgment of the platform’s users to resolve disputes between employees and employers. A number of users, randomly selected to prevent collusion, review the dispute and register their vote on the blockchain. A smart contract takes the final action based on the tally.

Decentralized ownership of the platform

One of the unique and valuable characteristics of blockchain-based freelancing platforms is the mutual ownership of the network. Centralized services run on top-down hierarchies, where the service provider holds sway over the application, data and everything else. In contrast, blockchain-based services rely on distributed, bottom-up organizations.

Most blockchain projects get their support from initial coin offerings (ICO), where startups issue proprietary cryptotokens to raise funds for their application. Enthusiasts and future users of the platform can invest in the project by purchasing tokens. Tokens give their holders a share in the ownership of the platform and can decide on its future. This mutual ownership ensures that everyone has a stake in seeing the platform rise in value and adoption.

Challenges remain

While blockchain solves many of the problems of online gig economy, it does have its own set of challenges and risks. This includes the fluctuating prices of cryptocurrencies, lack of centralized policing against fraud and scams as well as scaling issues attributed to blockchain platforms.

Startups have worked out some of these problems. For instance, CanYa uses a hedged escrow mechanism to protect employers and employees against token value changes after a contract starts. It also uses a combination of on-chain transactions and off-chain listings to improve performance and scale. Other platforms use decentralized computational resources to deal with application scaling. Coinlancer uses custom monitoring software to detect scams and enables users to flag potentially fake reviews.

What’s clear is that the blockchain business model, which incentivizes cooperation instead of competition, is very well suited for the online labor market, where everyone deserves to be rewarded fairly for their contribution.

Get the TNW newsletter

Get the most important tech news in your inbox each week.