GoBank, the self-proclaimed first truly mobile bank, today emerged from beta with general availability to the public.

Considering that most banks have moved toward releasing mobile applications for their products, GoBank’s distinction as a mobile bank isn’t functionally groundbreaking, but it does represent a shift toward a new generation of financial services. GoBank, the first new bank approved by the Federal Reserve since 2007, boasts that it was built from the ground up with smartphone banking in mind.

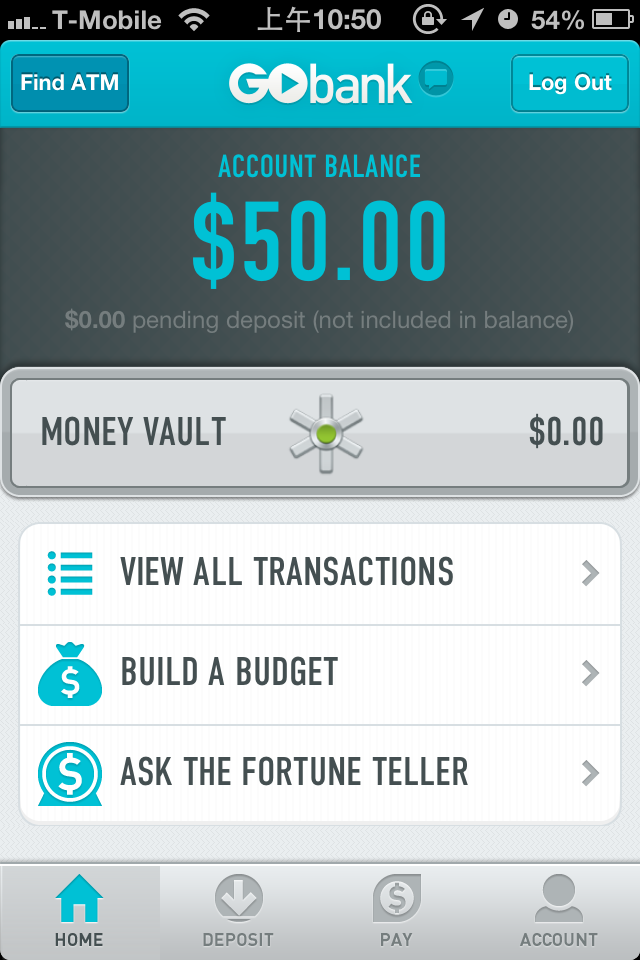

One benefit to going mobile is that you can sign up for a GoBank account straight from your phone, or you can register on the Web. The iOS app supports new customer accounts and a forthcoming update will add the feature to Android. The tradeoff is that there aren’t any physical branches if you prefer having the option to bank in person.

GoBank’s fee structure is also a draw. The membership fee is optional, in that users can select from a sliding scale ranging from $0 to $9. Over 42,000 ATMs nationwide can be used without charges and GoBank doesn’t have any overdraft fees.

Setting up my GoBank account was simple, and transferring money over from the account linked to my existing debit card was painless. I chose a free GoBank debit card (instead of a premium personalized version) and it arrived in the mail within days.

The <3 of EU tech

The latest rumblings from the EU tech scene, a story from our wise ol' founder Boris, and some questionable AI art. It's free, every week, in your inbox. Sign up now!

While GoBank meets all my regular banking needs, I can’t quite convince myself to use it as my primary bank. The thought of managing all my money on my phone, without any physical locations to fall back on, doesn’t put me at ease. I’m willing to admit that’s an irrational fear, as GoBank is FDIC-insured, and I hate going to an actual bank anyway.

GoBank’s VP of Product Development, Alok Deshpande, told me in an interview the bank had found that consumers have a lot of unnecessary pain and friction surrounding their accounts. However, I’ve settled into a reluctant rhythm with my bank. Most of the services I use are free and I rarely have to interact with the organization itself. As such, this isn’t a pain point for me.

Given the amount of complaining I hear about banking, there should theoretically be plenty of customers dissatisfied enough with their current accounts to make the switch, but I suspect that consumers will prove fairly resistant to changing banks. With our life savings at stake, it’s a weighty decision.

We put a lot of trust in our banks, so it will take some time for a newcomer on the scene to win customers over. When I asked about security, Deshpande reassured that the company has complied with “all industry best practices around keeping information and data safe and secure.”

Maybe I’m being too hard on GoBank, but I can’t shake the feeling that the company is ahead of its time. I’d bet money that physical banks will eventually become a novelty, but that doesn’t mean I’m willing to be a financial early adopter.

In the end, GoBank sits somewhere between traditional banks solutions and lighter newcomers like Simple, which isn’t actually a bank. I might not be ready for it, but you can decide for yourself now that it’s open to the public.

Image credit: iStockphoto

Get the TNW newsletter

Get the most important tech news in your inbox each week.