Like most people, I left college perplexed about how I was supposed to survive financially. I’d certainly left my alma mater with enough education — two full degrees under my belt — but also with a sizable portion of student debt. And, since I have made the boneheaded mistake of living in not one but two of the most expensive cities in the country (New York City and San Francisco) while scraping together money from journalism jobs, saving what little money I have has seemed like a far off dream.

Which is why, particularly in the last few months, I had a revelation: if I rely on apps to disrupt my life — pick me up from my house, deliver me ramen, find a cheap room to stay on vacation — why not use it to disrupt my finances?

So, as a semi-experiment and also a conscientious decision to make the leap and start making my money work for me, I decided to figure out if I could make my money work for me.

Here’s a short list of the ways I tried to use apps to save money. This list isn’t exhaustive and not everything worked for me, but exploring these options might make you into a money wizard, too.

Budgeting

Budgeting sounds easy in theory but is remarkably tough to accomplish in practice. Although I am friends with several people who have managed to turn receipt tabulating, cash flow tracking and savings plans into easy and very adult-like spreadsheets, I will admit that the time intensity and lack of direction (aside from “save money”) of the prospect has always turned me off. So, naturally, I looked to apps to cure my woes.

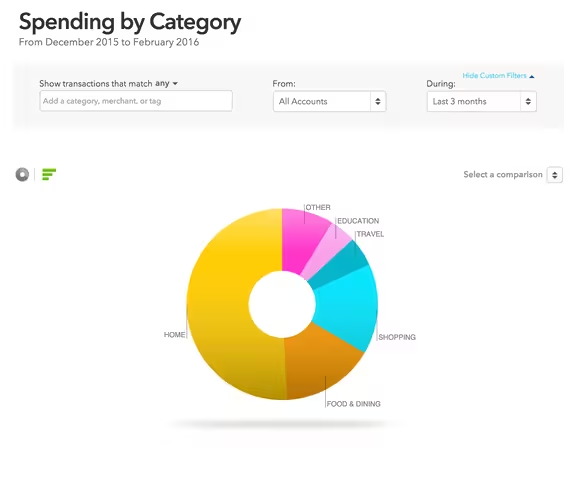

I have had Intuit budgeting product Mint for years now, with varying degrees of consistency and success. I returned to it in earnest to reorganize my spending habits and better understand where my money was coming from.

The best part of Mint is that it takes just a few taps to set up — the platform automatically registers and categorizes charges made to your debit and credit card, and dutifully keeps track of debt like student loans, as well as car and house payments. It also is the home of my credit score and my investment portfolio (more on that later), so I like the fact that I can get a quick overview of all of my finances instantly, and see where and how money is moving across different streams.

One downside, though, is that the platform isn’t necessarily very smart about compensating for non-expenditure transfers. For example: as part of my strategy to pay myself first, I automatically deposit $500 into my savings account as a baseline. Although that money didn’t technically move, it can incorrectly show up as a charge or make my budget wonky. Similarly, when I hooked up my Venmo and Paypal accounts — which I use particularly to move money around between friends and pay my bills — Mint can’t reconcile when they tap both the app and my checking account.

It’s not perfect but it does help map my spending, at least somewhat. But I decided I wanted to go deeper down the rabbit hole to become more savvy with my finances.

That’s how I ran into You Need a Budget — a longstanding and beloved software program that recently switched to a cloud-based offering designed to kick people’s financial asses into gear. Propelled by the idea that every dollar has a job, YNAB is for those who need to strictly, religiously allocate money to pay off debt, save quickly, or just get their house in order. The company also offers free classes, which are worth taking if you, like me, had literally no clue what to do.

Because I had a small savings stash already, it was difficult initially sorting out exactly how much I could really conceivably spend. Thanks to guidance from my Mint, I could tabulate monthly spending and route all the rest of my money to savings. But it requires dedication — if you are diligent and thoughtful enough to allocate funds, then you’ll likely get more value than if you’re laid back.

Saving

In addition to getting control of spending, I also wanted to save as much money as possible. While most of this was initially accomplished by the idea of paying myself first, I started thinking about how I could find and utilize savings I possibly didn’t know I had.

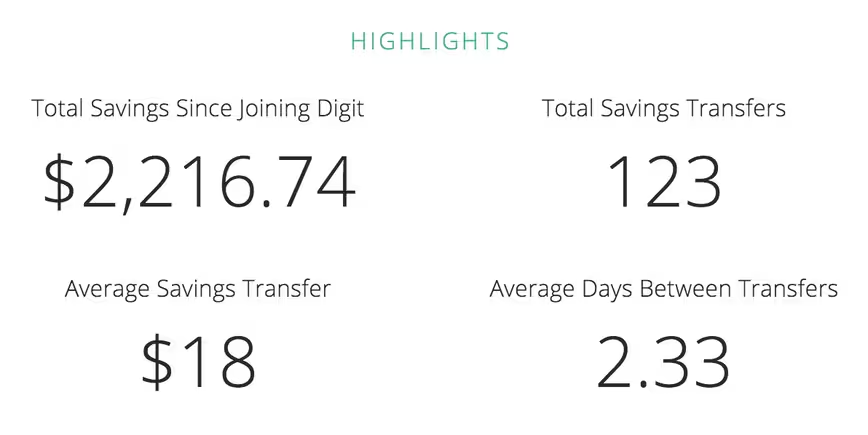

That’s why I turned to Digit in the first place. While I made deliberate savings transfers to build up my savings, this text-based app monitored my cash flow and siphoned away money when I wasn’t looking. Depending on my pay cycle, Digit would either sneak away between $2-$10 (enough to buy a nice cup of coffee or a decent lunch) or abscond with $50 or more.

And because I didn’t notice it, I didn’t miss it. Although Digit attempts to stay top-of-mind with daily Checking account updates, alerts when big cash deposits or withdrawals are made, and reports savings weekly, it was easier for me to just not think about it. I could sit back and let the app do the work.

This proved to be very successful. In addition to the money I could deliberately save mid-month and siphoning the rollover back into savings, I felt really good plunking down a hundred or two from Digit back into my account. For some months, if I felt a little extra “treat yo self” vibes, it didn’t feel wrong to allocate Digit as “fun money” that I could reward myself with. Other months, it could top off bills.

But frequently, it went into savings. And I didn’t have to do anything different in order to make it happen.

Investing

The final, “adult” step in my plan was to finally make all of this money work for me even after it was saved. For that, I decided to take off the training wheels and begin investing my money in a stocks and bonds portfolio.

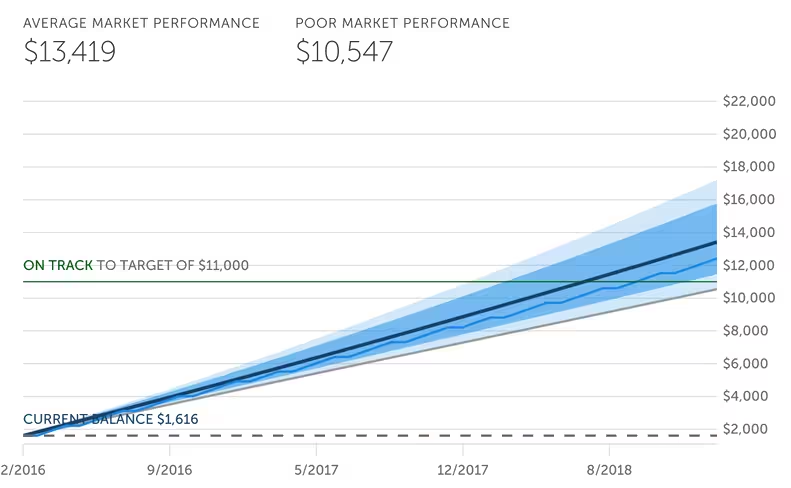

Now, to be completely honest, I’m not familiar with the nuances of the stock market, and beyond the principle that I needed to diversify where I invest my money, I had no idea where to start. So I decided to trust in word of mouth and open an account with Betterment. Relying on algorithms designed for goal-oriented saving, what I liked about Betterment was that it fine-tunes the percentage of stocks and bonds without much need for extra tweaking.

It also worked complementary to Mint and Digit, which I found to be a plus. In short, I allocated a flat amount of savings to put in my Betterment every month through auto-invest, and then allow the app to scan my savings for extra savings throughout the month. If my savings and my Digit harvesting were fruitful, Betterment would note the change and take up to hundreds of dollars more to invest on my behalf. All of this could be connected back to my Mint, which meant that I could look at it all from one clean dashboard without having to hop around.

Not bad.

Of course, some might not be interested in Betterment — I found it to be a happy middle ground based on my needs, but there are others to consider. A bit more old school, Vanguard has become a beloved name for finance nerds and has had great yields — though it is hidden under a slightly intimidating interface. For those who prefer a more laid back, bit-by-bit approach to investing, Acorns has similar mechanics to Digit but drops the spare change into an investment portfolio instead of a savings account.

The Future

This is my toolkit now, but that hasn’t stopped me from thinking about integrating more financial programs into my plans. For instance, if I feel confident in having a good fallback savings as well as a long-term safety net that could potentially build wealth over time, I might begin to eye an on-demand financial planning service like Wealthfront or LearnVest to help better understand the best ways to plan for the important things in life, like buying a house.

Additionally, I haven’t sworn off of more aggressive stock plans. If I decide to actually buy individual stocks, I would likely consider Robinhood to handle my trading simply and without fees.

But that’s a future I’m building towards. In my process of embracing financial technology, I’ve found that I feel more in control of my money and more comfortable with my cash flow. As I continue in my tactics — namely, to put hard caps on spending and dedicate money towards savings accounts and no where else — I feel like I have enough monitoring and planning at my disposal to make the whole thing less painful.

Swimming pool full of dollar bills, here I come.

Get the TNW newsletter

Get the most important tech news in your inbox each week.