Crowdsourcing pretty much anything is standard fare nowadays. At the end of last year, we brought you news of Crowdestates, a startup that wants to crowdfund the cash for people’s home improvements – before ultimately moving up to offering full mortgage amounts.

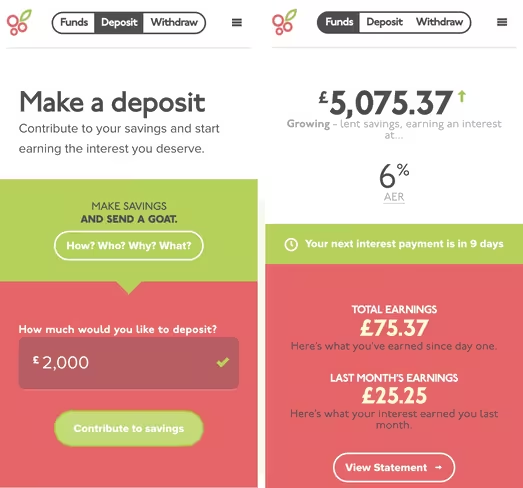

Another new entrant in the peer-to-peer lending space is Liverpool-based Fruitful, a platform that’s promising around 6 percent interest rates on money people choose to invest with the platform. That money is then lent out to people wanting to take out investment, development or commercial mortgages against properties.

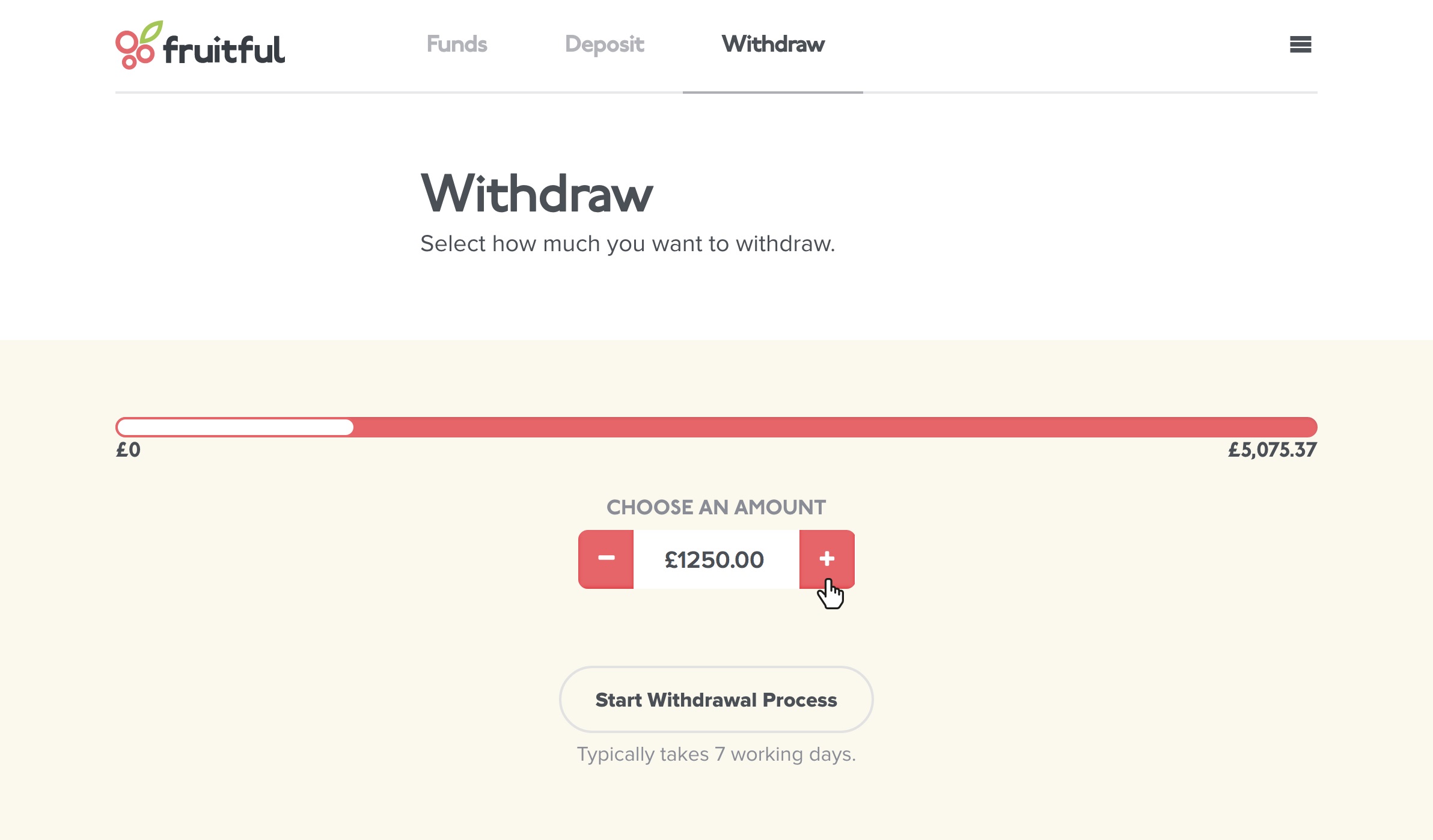

It’s a pretty simple equation: lenders provide up to £1 million that borrowers can use to put towards properties. Fruitful acts as the middle-man, thereby cutting banks out of the equation entirely.

Luke Barnes, founder or Fruitful, says: “Banks were once an important feature of a healthy economy. They offered savers fair returns, transactions were simple, they were principled and did good with their money.” That’s the sort of service that Barnes now wants Fruitful to provide.

To date, it has privately raised £500,000 of seed stage capital and is in the process of on-boarding customers who signed up for early access to the service.

With discontent and distrust in the banking system, a platform like Fruitful that offers everyday savers bank-beating interest rates will likely prove an attractive prospect.

To show its ethical side, Fruitful has also partnered with the Send a Cow charity in Africa to buy a dairy goat in exchange for every saver who deposits £1,000 or more.

On the borrowing side of things, in one way it’s a disappointment that the company is only helping existing businesses and commercial property developers (as this contributes to increasingly unaffordable housing) to take out loans, but it’s also understandable that a fledgling financial platform would want to secure users’ money against relatively stable brick-and-mortar investments.

Tom Darlow, Director of Product at Fruitful told TNW that offering residential mortgages is in fact on the company’s aim of long-term goals, but that the market is far more complex.

He also pointed out that “the small to medium-sized enterprises we’re lending to are in the same situation as individuals in the UK. Principally, good, creditworthy borrowers are unable to obtain finance through conventional banks, leaving them with the single option of paying high rent.” It’s also actually due to the fact that commercial mortgages typically command a higher rate than residential mortgages that Fruitful can offer lenders such an attractive interest rate.

In spite of the sound reasoning and the fact that the company is fully compliant with the Data Protection Act and Financial Conduct Authority (FCA), there will likely be some hesitancy from both lenders and borrowers until it can establish a solid track record.

➤ Fruitful

Get the TNW newsletter

Get the most important tech news in your inbox each week.