An overwhelming majority of 2018’s criminally-connected cryptocurrency was ultimately laundered on basic online exchange services.

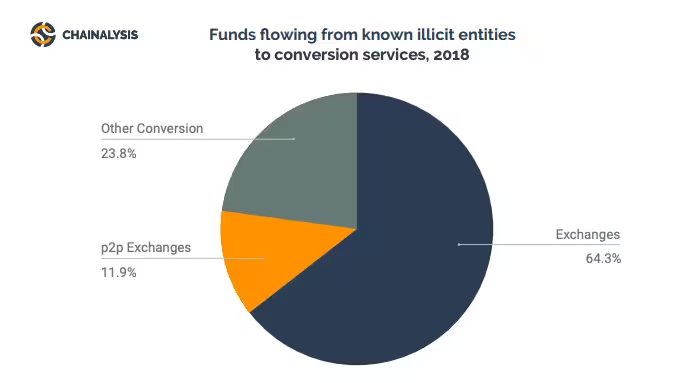

Blockchain researchers at Chainalysis have calculated that roughly 64 percent of last year’s dodgy cryptocurrency, which amounted to over $1 billion, was washed by simply depositing it onto digital asset exchanges and trading it.

Money launderers used other peer-to-peer (p2p) exchange services to clean a further 12 percent of their illegal proceeds.

This means over three-quarters of last year’s “illegal” cryptocurrency moved through an online exchange service at some point.

“A majority of illicit funds actually flow through either exchanges, or peer-to-peer exchanges, with the rest flowing through other conversion services such as mixing services, [Bitcoin] ATM’s and gambling sites,” declared Chainalysis.

Most of these digital funds were acquired by hacking cryptocurrency exchanges directly. Researchers noted that $36 million worth of Ethereum had also been stolen in 2018, typically through phishing, Ponzi schemes, or exit scams.

Tracking laundered cryptocurrency

The full report, which has been shared with Hard Fork, explains that with traditional currencies, “analysts can only estimate money laundering activity by working backward from successful prosecutions and making assumptions about how much of the total activity has been detected.”

But unlike fiat, which is extremely difficult to trace, cryptocurrency generally features transparent and complete transaction data, which allows new avenues for tracking and estimation.

“As in traditional currencies, money laundering in cryptocurrencies has three distinct phases: placement, layering, and integration,” explained Chainalysis. “Thus, a successful laundering scheme involves ‘placing’ criminal funds into the financial system, moving them around or ‘layering’ to avoid detection, and then ‘integrating’ those funds into the real economy, usually through a business, to make them look like legitimate profit.”

The investigators use special software to estimate funds being sent from tagged “illicit entities” to conversion services like mixers. This helps them quantify cryptocurrency money laundering, but doesn’t really give the full picture.

Chainalysis says a “significant amount” of criminal activity occurs off-chain, like when drug cartels exchange cryptocurrency directly to make cross-border payments.

“To investigate this form of money laundering would require anomaly detection software, the second of the necessary software […]. This software flags unusual activity that looks like ‘layering,’ for instance spikes in the frequency and size of transactions,” the report explained.

A regulatory nightmare for cryptocurrency exchanges

A little over $1 billion in illegal cryptocurrency is ultimately small change, especially considering Bitcoin‘s total transactional volume for 2018 was more than $410 billion.

Still, cryptocurrency exchange services and other businesses have already been forced to work together to appease government regulators hellbent on micro-managing the industry.

Just yesterday, four prominent exchanges announced they would be sharing transactional data in a bid to stamp out money laundering on their platforms.

So too affected are the cryptocurrency fat-cats looking to launch their Bitcoin-related Exchange Traded Funds (ETFs). On multiple occasions, the US Securities and Exchange Commission has promised it would not approve any ETFs on Wall Street unless it could be convinced that money laundering and market manipulation were no longer concerns.

In fact, the Winklevi’s Gemini exchange enlisted surveillance technology managed by financial giant NASDAQ to help prove it was up to the task.

Echoing this sentiment, Chainalysis urged that simple Know-Your-Customer (KYC) and Anti-Money-Laundering (AML) procedures will no longer cut it, and cryptocurrency exchanges should begin adopting what it calls Know-Your-Transaction (KYT) guidelines.

“KYT means cryptocurrency businesses and financial institutions can be informed about illicit activity so they can avoid getting involved in transactions that could harm them or their customers,” explained Chainalysis. “Automated cryptocurrency transaction monitoring is key to identifying patterns that indicate trouble spots and empower market participants to take action.”

So, with Know-Your-Customer, Anti-Money-Laundering, and now Know-Your-Transaction, one can’t help but wonder how far we are from making “Know-Your-Rights” the required rule instead.

Get the TNW newsletter

Get the most important tech news in your inbox each week.