I’ve been covering the nascent — and often weird — world of cryptocurrency and blockchain since January 2015.

During this time, I’ve seen banks dismiss the digital currency but declare their undying love for its underlying blockchain technology, and more recently open up about plans to possibly launch their own version.

I’ve witnessed the wild conspiracy theories, the proofs-of-concept, the crime, the hype — you name it, I’ve seen it, and probably even written about it.

Blockchain is clearly not the only emerging technology that’s gained momentum in recent years. Advancements in artificial intelligence or the internet-of-things, for example, have also received significant attention. But there’s something quite disconcerting about the way in which blockchain hype is portrayed.

Ugh, the hype

We’ve often heard the line that “blockchain is a solution looking for a problem” and in a way, I have to say I agree.

The notion of decentralization definitely seemed interesting in the aftermath of the 2008 financial crisis as consumers rightly lost trust in the banking system. But the question I’ve been asking myself for years is: what issues, or issues, is blockchain actually trying to solve? And why?

Some of its purported use cases (voting, payments, digital ID, supply chain management, etc) amount to little more than the willingness to add a distributed and encrypted ledger where one is not actually needed. It sometimes feels like blockchain is being thrown into the mix to complicate, rather than simplify, existing processes just because it’s trendy.

Meaningless

Although perhaps the real problem is that the term “blockchain” has become so widely used that it’s become somewhat redundant.

Writing for the Verge, Adrienne Jeffries, points out that “the idea of a blockchain, the cryptographically enhanced digital ledger that underpins Bitcoin and most cryptocurrencies, is now being used to describe everything from a system for inter-bank transactions to a new supply chain database for Walmart. The term has become so widespread that it’s quickly losing meaning.”

The lack of universal definition about what constitutes blockchain technology is likely a factor that’s also contributed to its lack of adoption. On a purely simplistic note, how can we apply a solution to a problem if we’re not quite sure about what the solution actually is?

Disillusionment

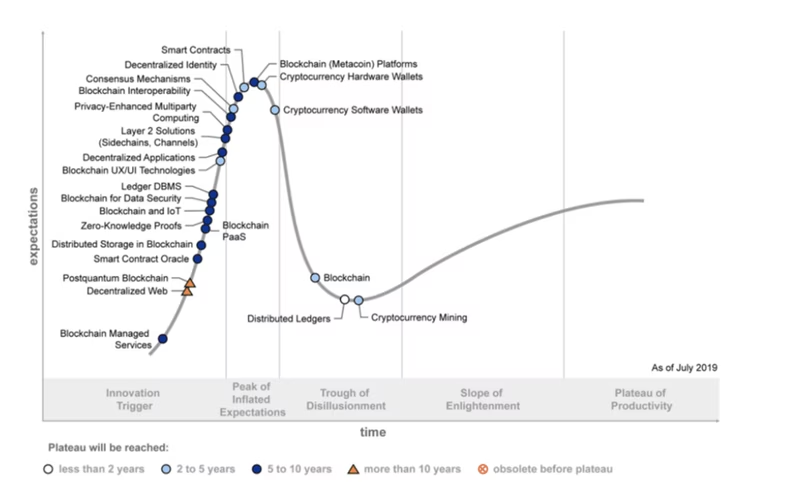

According to Gartner’s Hype Cycle, blockchain is still “sliding into the trough of disillusionment,” meaning the technology is struggling to live up to the expectations created by the hype around it.

The Hype Cycle shows that most blockchain technologies are still five to 10 years away from having transformational impact, but if memory doesn’t fail me, this has been the case for as long as I’ve been covering the space.

I can appreciate that it may take a while for some nascent technologies to mature and find their killer app, but surely the fact that it’s taken this long for blockchain to operate freely in the wild, is indicative of its potential future success — or lack thereof.

The wrong approach

Clearly not everyone agrees with me, though.

Antoine Poirson, a partner at Antler, an early-stage venture capital firm and startup builder, still believes blockchain could make it.

“If blockchain technology has been overhyped in the past, mainly because of the hype around cryptocurrencies which rely on this technology, it does have a lot of potential,” he said.

“Allowing trust to be created in a distributed manner remains very powerful, and a lot of broader use cases have started to emerge. Blockchain technology is an enabler for business model innovation, however, until the business cases have been identified, the potential of the technology is not fully utilized,” Poirson added.

Perhaps this is the crux of the issue: maybe blockchain technology hasn’t succeeded to date because the approach hasn’t been focused or specific enough.

Desperate to improve their bottom lines, corporates have tried to leverage the technology in a bid to maximize efficiency and save costs. Banks, for example, have widely explored blockchain‘s ability to improve the post-settlement and clearing process. On the other hand, corporates are still toying with the idea of using blockchain to track the provenance of goods or improve transparency.

Something bigger

Blockchain’s purported promise is such that everyone is willingly taking a multi-faceted approach, not giving much thought to the possibility that its potential may, in fact, be limited. Or maybe blockchain is just the first iteration of something far more powerful, a base we can build on to restore our faith in decentralized systems.

I’m aware that this article will not necessarily go down well with hardcore blockchain enthusiasts, and that’s fine. But, as we enter the new year, I urge you to take a moment and think about what lies ahead. How can we make the blockchain space different in 2020, and more importantly, what’s needed to enact this change?

Earlier this year, I wrote a piece titled “Hype is killing blockchain technology.” At the time, you could argue it was my attempt to re-assess the industry following a three-year hiatus, but fast forward 10 months and not much has changed.

Get the TNW newsletter

Get the most important tech news in your inbox each week.