Payment processing startup Ribbon launched a new product today aimed at helping independent contractors and individuals send money to one another. The company is taking on the likes of Square Cash, PayPal-owned Venmo, and other peer-to-peer payment services. It’s main selling point? You shouldn’t need an account to send money.

The product is free to use in the US and currently accepts dollars. However, in order to try it out, you’ll need to request an invite.

The consumer option joins alongside Ribbon Merchant, which lets businesses accept payments through their websites, YouTube, Facebook, and other social networks. But it isn’t all that surprising, as TechCrunch revealed plans for the peer-to-peer payment tool in November.

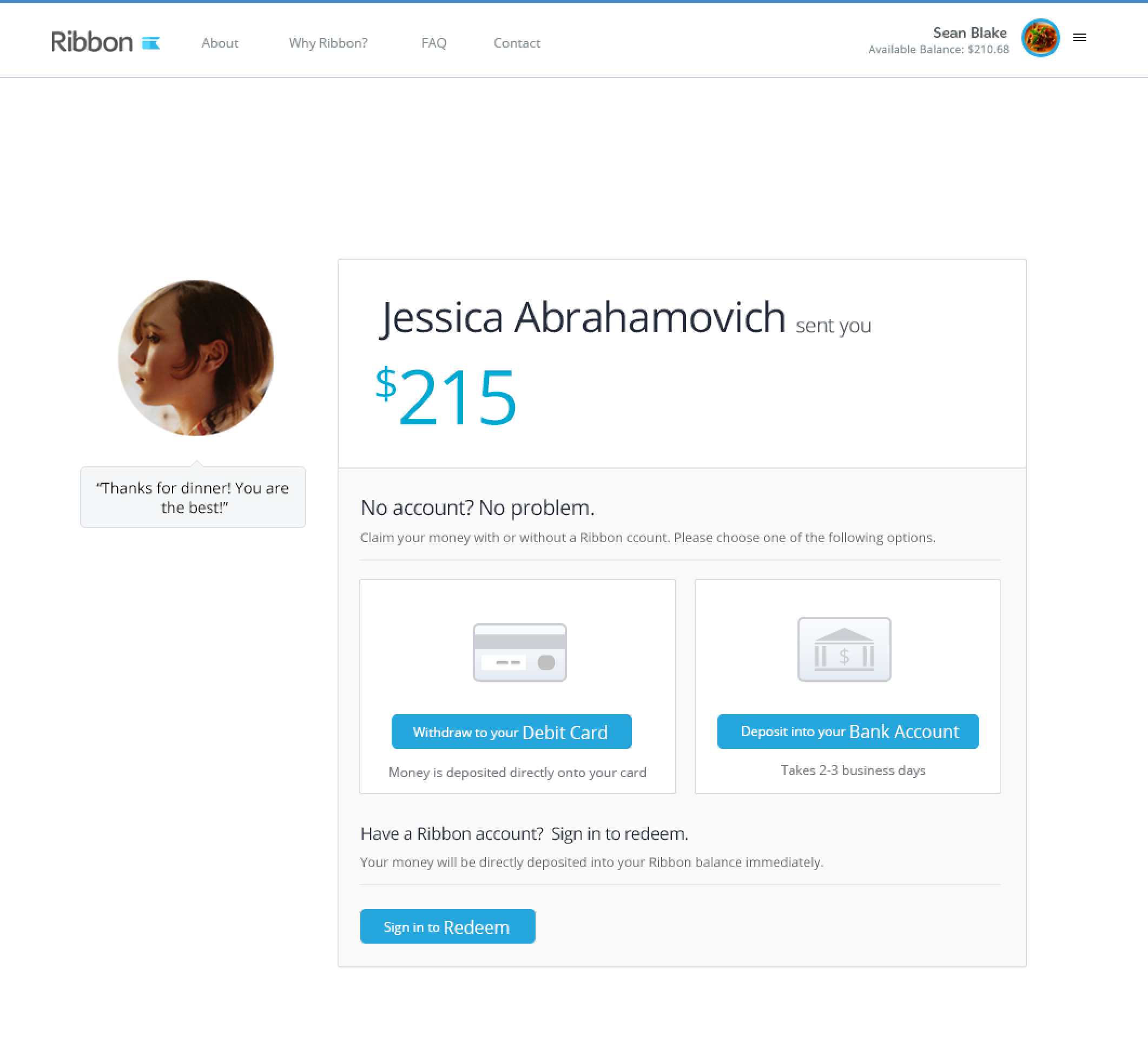

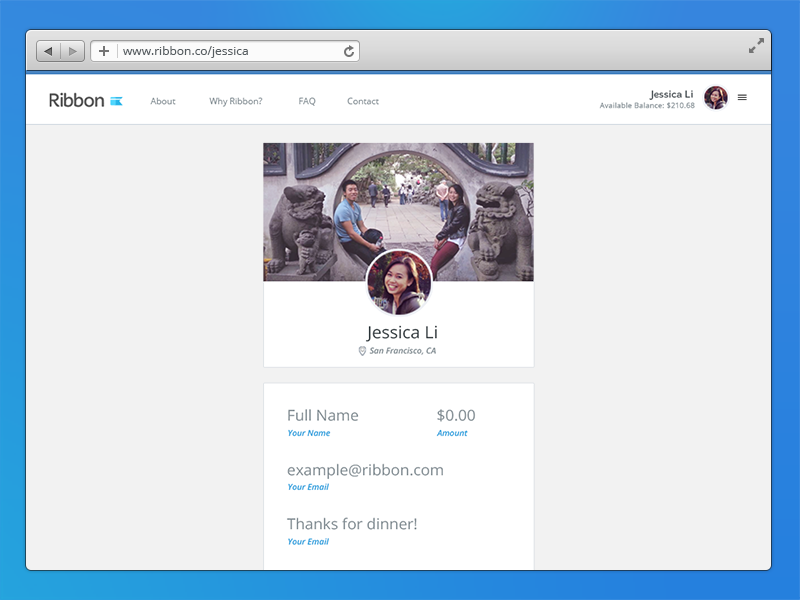

Consumers don’t need to download an app in order to use the product. You can simply send a URL like ribbon.com/[yourname] and the recipient will see a page with the standard Ribbon display. Simply enter in the amount you wish to send (there is a limit of $2,500 per week) and you’ll get a notification to pick up your money. You can also use the URL format ribbon.com/[yourname]/[dollar amount] where [dollar amount] will be pre-populated in the form, so if [dollar amount] is 25, then you’re charging the recipient $25.

Anyone can send/receive money through their bank account, debit, or credit card. However, if using a credit card, there is a 3 percent transaction fee imposed on the money sender.

Hany Rashwan, Ribbon’s CEO, tells us that this new consumer tool is easier and more powerful than Square Cash simply because you don’t need to have an account to send money — only the collector of the funds will need to have an account. He believes that forcing users to sign up for an account in order to complete the checkout process is a big hurdle for consumers (“Yet another account I have to sign up for.”) and results in two-thirds of people abandoning the process.

Ribbon originally launched as a platform to allow anyone to sell items on the Internet. However, Rashwan noticed that there were some individuals that were using a workaround on Ribbon to send money to their friends. Ribbon for Consumers gives users the capabilities that they need in a rather easy manner.

Previously, Rashwan and his team put most of their proverbial eggs in its merchant product, and it’s still in operation. Of course there were some bumps in the road. After successfully launching its integration with YouTube and Facebook, Ribbon stumbled when it released an update that supported Twitter Cards. The service was quickly shut down without any explanation. But two days later, things were back to normal.

The company has been testing this new product for the past few months with “hundreds” of beta testers.

Photo credit: Arif Ali/AFP/Getty Images

Get the TNW newsletter

Get the most important tech news in your inbox each week.